Summary

- Bears cite Hanesbrands' debt load and lack of tangible equity as justification for avoiding or shorting the shares. Over 20% of the float is shorted.

- Hanesbrands generates huge amount of free cash flow. A large part of the free cash flow is earmarked for deleveraging. Hanesbrands has been reducing its cost of debt.

- After a period of disruption in retail, Hanesbrands sales and EBITDA growth is stabilizing as the company adjusts to the new landscape. Revenues are increasing at a decent clip.

- I am unconvinced by the bear case that Hanesbrands is being disrupted by Amazon. I believe Hanesbrands provides compelling value.

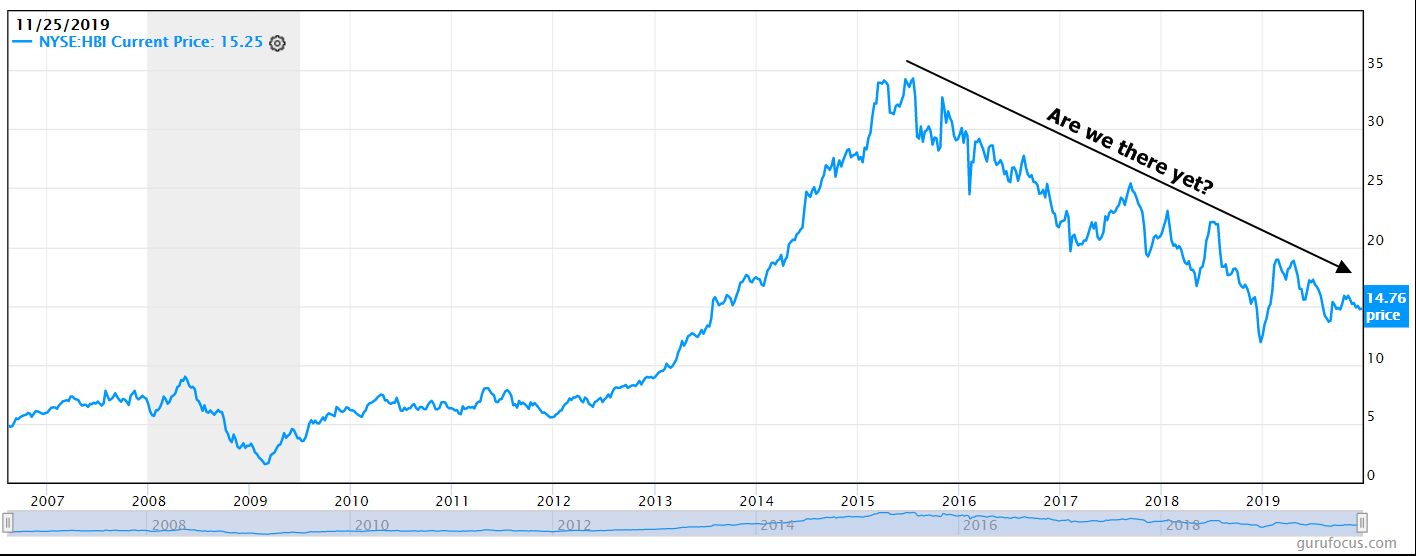

- However, the fact is that the stock has been in a downtrend for nearly five years now. The stock is down >50% from it peak (while the S&P 500 is up ~50% during this time). Is Hanesbrands a value trap?

It's safe to say that Hanesbrands (HBI) is unlikely to win a popularity contest among investors. Since peaking in 2015, the stock has been in a relentless downward channel. Currently short % of float is 20.15.

It's safe to say that Hanesbrands (HBI) is unlikely to win a popularity contest among investors. Since peaking in 2015, the stock has been in a relentless downward channel. Currently short % of float is 20.15.

Chart 1. Source: Gurufocus.com

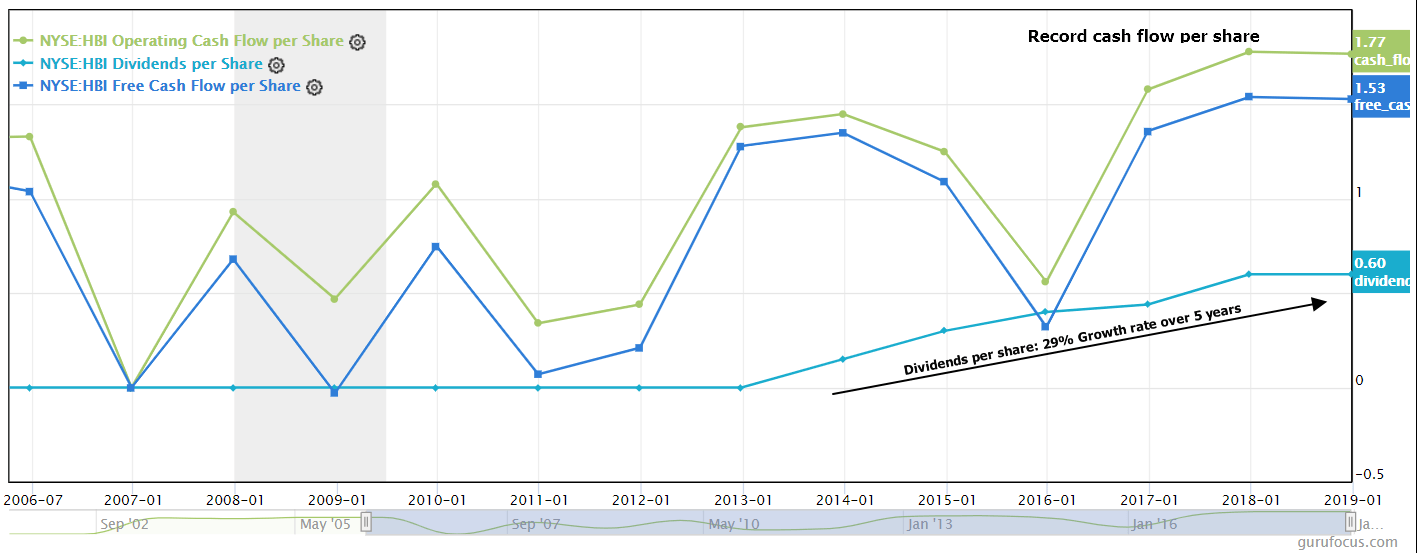

However, cash flow per share continues to grow nicely and dividends have increased at a terrific pace over the last five years. The company has however suspended dividend increases as it focuses on deleveraging.

Chart 2. Source: Gurufocus.com

Background

On September 5th, 2006, Sara Lee Corporation spun off its branded clothing Americas and Asia business as a separate company called Hanesbrands Inc., which designs, manufactures, sources and sells a broad range of clothing essentials. As part of the spinoff, the company's balance sheet was highly leveraged with $2.6 Billion in debt. This debt was used to pay a $2.4 Billion dividend to Sara Lee. The HBI shares were distributed to Sara Lee shareholders.

The company's portfolio of brands include Hanes (its largest brand), Champion (its second largest brand), Playtex (its third largest brand), Bali, Just My Size, Barely There, Wonderbra, L'eggs, C9 by Champion, Duofold, Beefy-T, Outer Banks, Sol y Oro, Rinbros, Zorba and Ritmo. Target (NYSE:TGT) recently discontinued carrying C9 by Champion brand.

Since its 2006 IPO, Hanesbrands has acquired a number of businesses.

| Acquiree Name | Announced Date | Price |

| Bras N Things | 8-Feb-18 | $400M |

| Alternative Apparel | 18-Oct-17 | $60M |

| Pacific Brands | 27-Apr-16 | $800M |

| Champion Europe | 7-Apr-16 | ? |

| Knights Apparel | 24-Feb-15 | ? |

| DBApparel | 25-Jun-14 | $528M |

| Maidenform | 24-Jul-13 | ? |

| TNF Group | 6-Mar-11 | ? |

| Gear for Sports | 1-Nov-10 | ? |

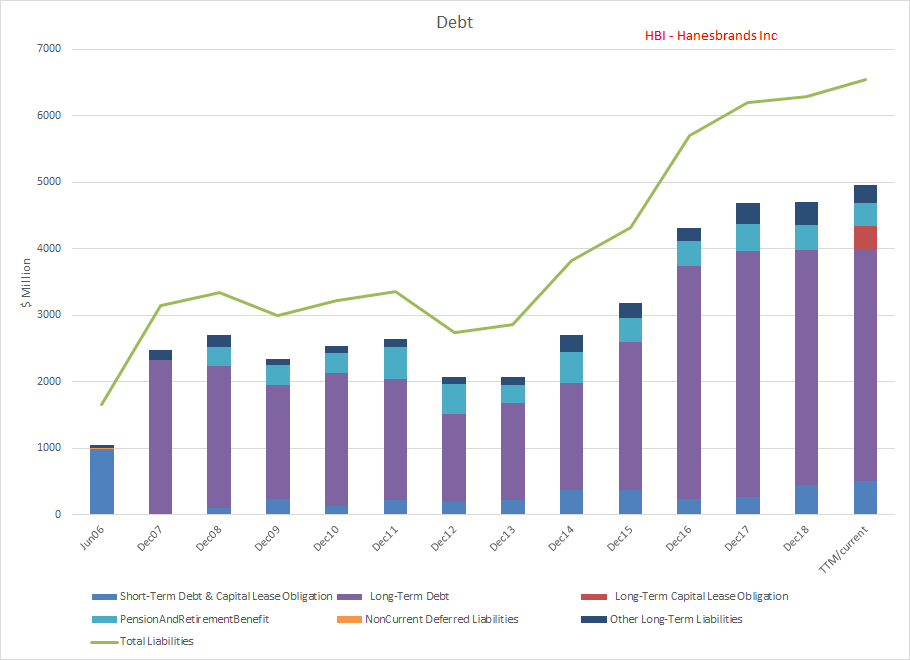

Chart 3.

Debt

All these acquisitions have added to debt. The company in addition has bought back over 40 million shares since 2015. Lately the company has turned its attention to de-leveraging, correctly perceiving that investors are nervous about the debt given seismic changes in the retail landscape and the sense that we may be coming to the end of this business cycle.

Chart 4. Source: Author with data from Gurufocus.com