Summary

- RYAM has renegotiated debt covenants so its likely safe from bankruptcy for a couple of years.

- It has sold a pulp paper mill and is now focused on cost cutting. It was also forced by debt holders into cutting its dividends.

- Given past poor capital allocation decisions and high debt burden, the survival of the company depends on the improvement in the specialty cellulose market.

- Investors should be under no illusion that RYAM is a price taker operating in a commodity market with no moat.

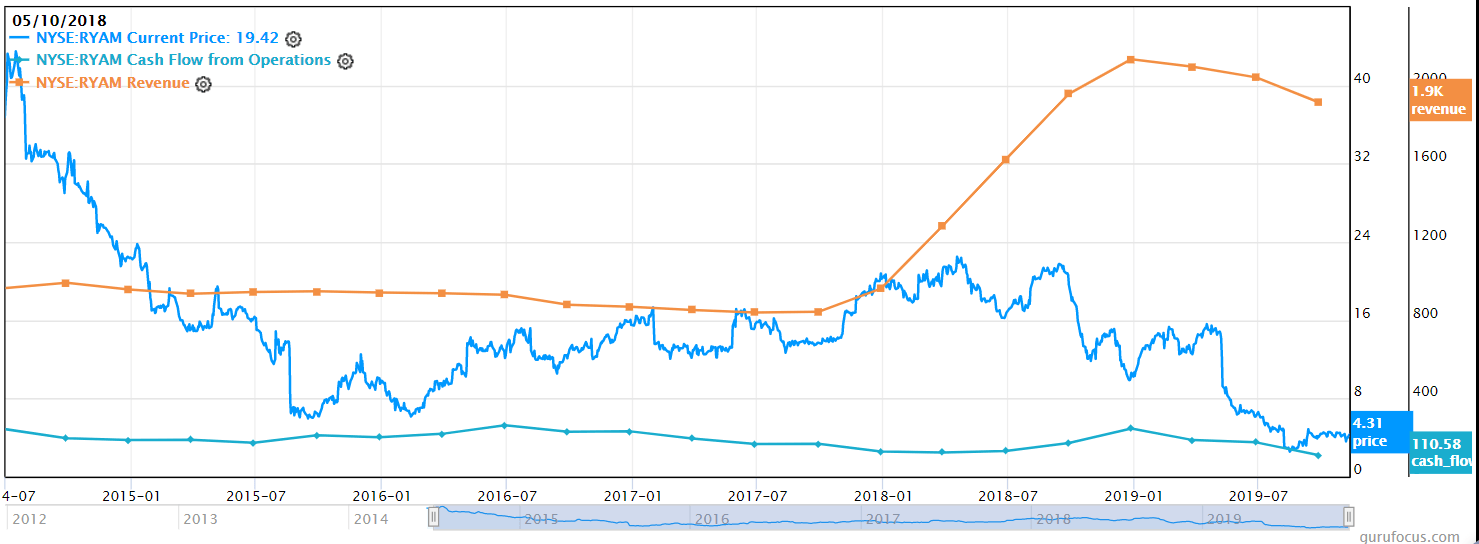

Rayonier Advanced Materials Inc.'s (NYSE:RYAM) main business is manufacturing high-purity cellulose, a natural polymer derived from wood pulp, used by its customers to make cigarette filters, cell phones, flat-panel televisions, tires, rayon fabrics, paint and pharmaceuticals, among other things. It was spun out of Rayonier (RYN) in mid-2014 which became a pure-play forest REIT. The spin-off was pitched to investors that the cellulose speciality that the company made was difficult to make, it was a long time leader in a recession-resistant business with an entrenched position and this expertise in cellulose specialities forms a moat around its business.

As part of the spin out the parent, Rayonier extracted value by loading down RYAM with debt. Soon after IPO, RYAM went through a difficult period as management made some really bad capital allocation decisions expanding capacity in high purity cellulose while the bottom fell out of prices due to industry over capacity and lack of demand. The stock crashed from over $40 a share in September 2014 to around $6 in September 2015.

RYAM acquired Quebec, Canada-based quasi-competitor Tembec in May 2017 for $807 million. Acquisition of Tembec diversified RYAM away from high purity cellulose towards commodity cellulose, forest products, and pulp and paper. However this has not gone according to plan. The acquisition coincided with a general downturn in the forest products market. This has caused significant erosion in operating margins of the company.

Source: Gurufocus

Earlier this year RYAM came close to breaching some debt covenants and was forced to negotiate with its lenders for relief. This crashed the stock further to below $3, on bankruptcy fears. On September 30th the company announced that did manage to negotiate relaxation of covenant terms till 2021 buying itself some breathing room at the cost of 1.25% increase in interest rates and increased collateral. It also sold it pulp mill in Quebec (acquired with Tembec) for $150 million and used $100 million of the proceeds to reduce debt. The company was also forced to suspend its dividend for its common shares.

The company's preferred stock converted to common in August with 13.4 million new common shares issues bringing total shares outstanding to over 63 million diluting the common stockholders by ~21%. However the company does save the preferred dividends.