Summary

- The stock has dropped over 15 points from its recent highs, and we think there will be support just under $150, a level we find compelling.

- At the low end of our EPS expectations, AAP shares are historically heavily discounted.

- Longer-term this stock could see growth of another 100 points, while we believe downside is limited to about 20% according to our calculations.

- Looking for a helping hand in the market? Members of BAD BEAT Investing get exclusive ideas and guidance to navigate any climate. Get started today »

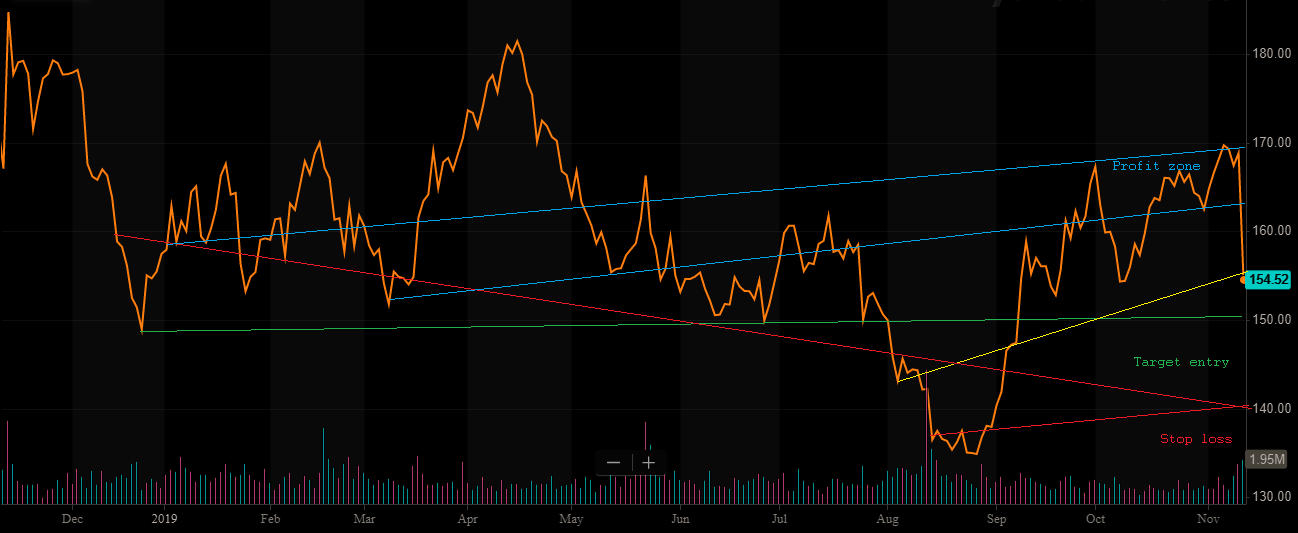

One of our best recommendations was on AutoZone (AZO), and with that we have done a lot of due diligence in the auto parts sector, and know it quite well. A few months ago we recommended its competitor Advance Auto Parts (AAP) and we said it was a buy at $150 with a target exit of $170. That level was reached earlier this month, and now, it is on our radar again after nosediving following a better-than-expected Q3 result. We think you can let it fall, then scoop some shares up for a rapid-return trade.

The stock has dropped over 15 points from its recent highs, and we think there will be support just under $150, a level we find compelling. We expect to be able to pick up a few points on this play quite easily, so long as it falls to the levels of interest. The stock had seen some solid growth long term, but has been very tradeable in recent months but has fallen off of late. We believe there is an opportunity here. Here is the one-year chart:

Source: BAD BEAT Investing

We see an opportunity between $140 and $150 to scoop up some shares. These are the levels we suggest a buy at. We will keep a tight stop on this one and look to scalp some gains. If you opt to play options here we would either sell puts to raise some cash or do a longer dated call, given the somewhat tight range of the stock.