Summary

- Were I to make bets on specific players relative to the overall banking space, I think Bank of America would be a good name to consider.

- Supporting my mildly bullish position is the bank's solid balance sheet and a better-balanced business model.

- I believe BAC could be a good "middle-of-the-road" option for investors looking for a bit more high-quality bargain in the banking space.

- Looking for a helping hand in the market? Members of Storm-Resistant Growth get exclusive ideas and guidance to navigate any climate. Get started today »

I have written a bit recently about how eventful I expect earnings season to be for financial service companies. The sector has been grappling with a number of (largely unfavorable) macroeconomic events, including the escalation of the U.S.-China trade wars and decreasing interest rates, along with industry-specific trends that bode ill for M&A and trading activity.

For these reasons and considering what I and many other analysts perceive to be the tail end of the decade-long economic expansionary cycle, I do not think that a heavier portfolio allocation towards the financial services sector makes much sense at current levels. But were I to make bets on specific players relative to the overall space, I continue to think that Bank of America (BAC) would be a good name to consider.

Credit: Ben's Bargains

Over the past two years or so since I singled out BAC as a potential winner in the mega bank sub-sector, the stock has performed better than the industry average and even the S&P 500 (SPY) - along with my top pick in banking, JPMorgan (JPM). While the strong global economy helped to lift all boats in the first three quarters of last year, I believe Bank of America and JPMorgan stood out once interest rates began to move against the sector and concerns over the macroeconomic landscape began to surface.

Part of the reason for the stock's decent performance, in my view, is the quality of Bank of America's balance sheet. On the consumer side of the business, the net charge off ratio has been declining in the past few quarters, while delinquencies having been trending substantially lower - 0.96% of total outstanding loans were past due 30 days or more in 2Q19 vs. 1.28% in the comparable quarter last year. For reference, delinquencies have been trending higher instead across the industry.

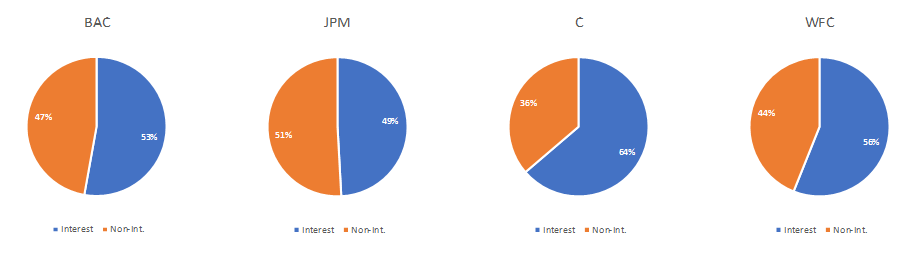

Source: DM Martins Research, using data from multiple company reports

But I also believe Bank of America's business to be better balanced than those of peers Citigroup (C) and Wells Fargo (WFC), for example. As the charts above depict, nearly half of the Charlotte-based bank's total revenues are fee-based. As a result, the bank has theoretically been less exposed than Citi or Wells Fargo to swings in interest rates, which tends to add uncertainty to banks' financial performance.

Also, about 62% of the Bank of America's revenues come from the consumer and wealth management sides of the business, which I consider good exposure to the one component of the U.S economy that remains healthy: consumer spending. For reference, Citigroup produces more than half of its revenues from institutional clients, a business model that can suffer most from continued softness in investment banking, fixed income, and equity trading.