Summary

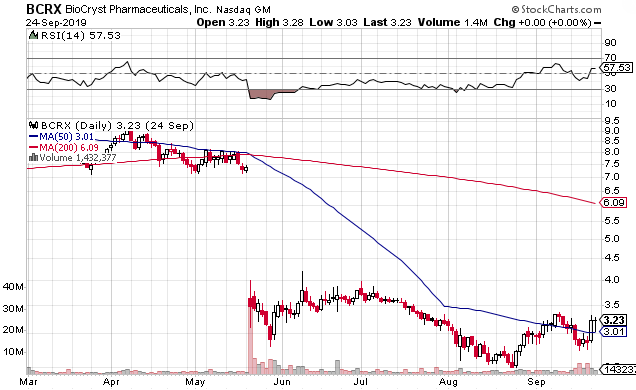

- Shares of BioCryst are stuck around $3 per share since the stock plunged after the company reported phase 3 results of BCX7353 in HAE patients.

- The company's cash balance will soon decline to dangerous levels - a cash infusion is badly needed in the next few months.

- I am doubtful of BCX7353's market potential, but management remains optimistic and is talking up its selling points.

- BCX9930 phase 1 results are due before year-end, and Achillion set a high bar with ACH-5228.

- I remain interested but on the sidelines at least until the company raises enough cash to last into 2021.

- I do much more than just articles at Growth Stock Forum: Members get access to model portfolios, regular updates, a chat room, and more. Get started today »

Shares of BioCryst Pharmaceuticals (BCRX) are stuck around $3 per share ever since the stock plunged after reporting phase 3 results of BCX7353 in hereditary angioedema (‘HAE’) in May. The subpar phase 3 results (relative to an available competing therapy) and the company’s poor financial situation are mostly to blame. BioCryst ended Q2 with only $97.5 million in cash and equivalents, and a projected cash burn for 2019 in the $105 million to $130 million range suggests the company needs to raise cash soon. I continue to believe that BCX7353 is a weak competitor to Takhzyro, and I also have doubts about the company’s ability to get to a position where it can try to compete without hurting shareholders in a meaningful way – be it with debt it may not be able to service, or with significant dilution.

Source: Stockcharts.com

On the other hand, I continue to have interest in the company’s factor D inhibitor BCX9930 and look forward to seeing the phase 1 results in healthy volunteers which should provide insight about its potential to compete with Achillion’s (NASDAQ:ACHN) first and second-gen factor D inhibitors. I remain on the sidelines for the time being but interested in seeing how this story develops in the following months.

BioCryst needs to raise cash soon

As mentioned, BioCryst ended Q2 2019 with $97.5 million in cash and equivalents, a $30.9 million decrease compared to the first quarter. The company continues to guide for operating cash utilization for 2019 in the $105-130 million range, which suggests a burn rate in the $50-75 million range in the second half of the year. Waiting much longer may result in further share price weakness and result in the risk of the company not being able to utilize equity as a means of raising (enough) cash.

BioCryst announced last week that it had entered into an amendment of the credit agreement with MidCap under which it has extended the deadline for drawing the second $30 million tranche by November 30, 2019. But even if BioCryst elects to draw the additional $30 million, it merely represents a one quarter lifeline. The credit agreement allows the company to draw $20 million more, but only after BCX7353’s FDA approval. The company can’t wait that long without raising additional cash in the meantime.

Management said on the Q2 earnings call and at two investor conferences earlier this month that equity and debt are being considered, including royalty-backed debt. Extending the cash runway into 2021 would be desirable, which suggests BioCryst needs to raise at least $100 million and be able to draw at least $30 million out of the $50 million available under the MidCap credit facility.

I will not consider taking a position in BioCryst until sufficient cash is secured.