Summary

- Israel’s Teva Pharmaceutical Industries Ltd. share price sells a notch above its 19 years low. Investor sentiment is low too. I do not recommend retail investors buy this stock now.

- TEVA still has significant though more manageable debt through drastic measures. It remains exposed to legal liabilities related to the opioid crisis and U.S. charges of price-fixing of pharmaceuticals.

- TEVA's entry into the cannabis market by distributing other companies' products makes for headlines but adds nothing significant to the behemoth's revenues and earnings. It distracts from the core business.

- Daniel Goldmeier of Goldmeier Investments assisted in writing this article.

Too Much Risk Too Soon

Israel's Teva Pharmaceutical Industries Ltd. (TEVA) share price sells a notch above its 19 years low. Yet, I do not recommend retail investors buy this stock now. The company has no major catalysts on the horizon. TEVA still has significant though more manageable debt. It remains exposed to legal liabilities related to the opioid crisis and U.S. charges of price-fixing of pharmaceuticals. In my opinion, given the high risk and low reward profile, retail investors have no business buying TEVA shares.

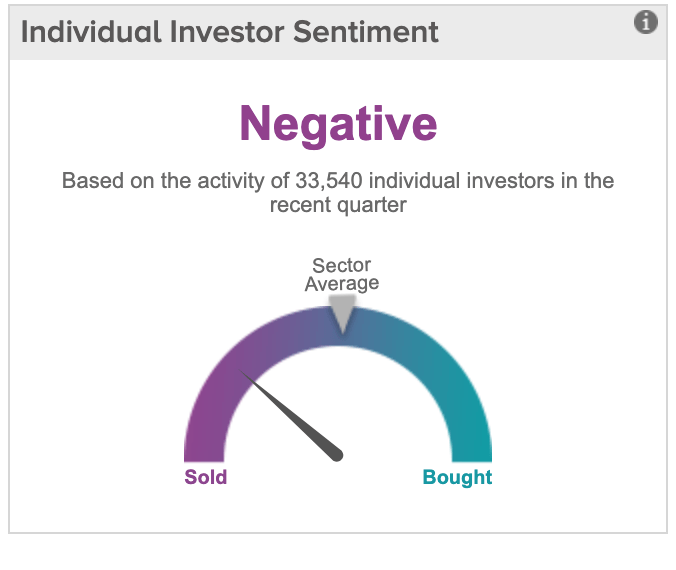

Source: Tipranks

Source: Tipranks

Accumulating Problems

Investor sentiment in TEVA is low. Share price hovers near a multi-year low despite new management's drastic efforts to rid TEVA of crushing debt and legal battles. TEVA may have to pay billions in accumulated legal fees for old and new cases. The cash, time and attention are better used to building its core business. Previous management engaged in a poorly executed and faulty business plan to grow Teva through overpriced friendly and hostile acquisitions. New management laid off 10,000 employees and is selling assets; that's not good for employee morale and retention of brainpower but management has few other choices.

Second, Warren Buffet's Berkshire Hathaway (BRK.A) (NYSE:BRK.B) reportedly owns 43M TEVA shares with a paper loss amounting to ~$300M. Retail investors need to heed Mr. Buffett's advice, i.e., never chase a hot stock up or buy one struggling to bounce back. TEVA is attempting to regain some of their hot stock glory by entering the medical marijuana space. For the foreseeable future, that decision will contribute negligibly to revenues and earnings. TEVA is distributing other firms' products and that is not a catalyst to drive TEVA share price higher.

My third reason for not recommending TEVA is management's dive into the medical cannabis arena is for apparent sake of appearances. Teva once was the imprimatur of the generic drug maker world. TEVA remains one of the largest pharma companies and maker of generic drugs in the world considering market cap and revenue. But do not be misled by screaming headlines this past summer like in Forbes touting TEVA making "A Big Move in Cannabis." It is not a big move, simply one that poses risk and minimal reward.