Summary

- A recent pullback in the packaging sector offers investors an opportunity.

- Sonoco Products Company is more diversified than peers but trades at a premium valuation.

- Investors can find higher yields, lower valuations, and higher upside elsewhere in the sector.

- After recent results, it is clear Sonoco does not deserve to trade at a premium.

![]()

Source: Sonoco.com

Sonoco Products Company (NYSE:SON) operates in the consumer packaging and goods space. It is a dividend aristocrat that can be counted on year after year to raise its payout in good times or bad. Investors like the company for its smaller market capitalization compared to peers and its diversified product offerings. While the company faces larger more well-capitalized peers, it offers stronger growth due to its product offerings. However, much of this appears to be priced in as the valuation trades at levels quite a bit higher than peers. This is despite the fact that the growth in the most recent quarter was less than inspiring. We review where shares would become an attractive investment and what peers offer better value.

Performance

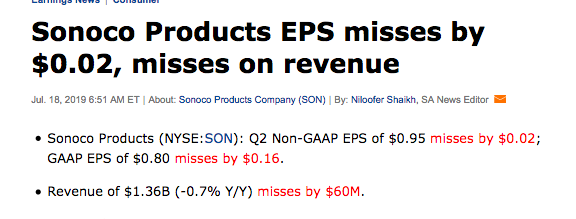

Sonoco recently reported earnings that missed on the top and bottom lines.

Source: Seeking Alpha

While I consider this miss negligible, it is the decline in revenues that appeared to be less than attractive. Furthermore, the company reported adjusted earnings per share that was the same as the year prior.

Source: Earnings Slides

Source: Earnings Slides

While net income saw growth, it was primarily due to a lower effective tax rate and lower S&A expenses. The company did, however, reaffirm guidance for the year to $3.52 to $3.62 per share. This represents roughly 14% growth at the midpoint of the guidance over 2018 earnings.

Looking at each division individually, we see that almost every divisions saw a decline and only one saw growth.