Summary

- VF Corp. has a stellar history of actively managing their portfolio of brands.

- The Jeans spin-off leaves VF Corp. as a more focused, faster-growing company.

- While investors are excited about its prospects, the company has been a large beneficiary of the ‘athleisure’ trend, and it appears the competitive environment will only intensify.

Introduction

V.F. Corp. (NYSE:VFC) has a stellar track-record of acquiring and managing a diverse portfolio of apparel brands. They purchased brands at attractive prices, invested behind them, and then prudently managed them over time. Most recently in May, they spun off the Jeans business (click here to see the list of recent spin-offs) which removed the slowest growing piece of the company. Without Jeans, VF Corp. should be a faster-growing, higher-margin business going forward.

History of Active Portfolio Management

VF Corp. has a track record of making savvy acquisitions and managing the underlying portfolio of brands over the last 20 years. Back in the late 1990s/early2000s, most of the business came from Jeans (Wrangler and Lee brands), Intimate Apparel (Vanity Fair, Lily of France, etc.), Occupational Apparel (Red Kap), and Outdoor Clothing and Equipment (Jansport). Today, these brands are either no longer with the company or account for a very small portion of overall sales.

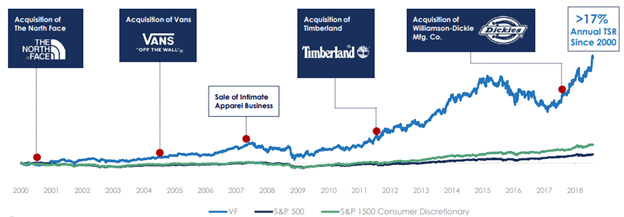

The seeds for VF Corp.'s current business were planted in the early-to-mid 2000s when they acquired two important brands. In 2000, they acquired The North Face for a little over $25 million when it was on the brink of bankruptcy, and then, in 2004, they acquired Vans for just under $400 million. These are their top two brands today and generate many billions of dollars of revenue. More recently, they acquired Timberland in 2011, Williamson-Dickie in 2017 for nearly $800 million, and two smaller brands, Icebreaker and Altra, in 2018.

VF Corp. has been able to grow acquired businesses through investing in advertising, sponsorships, line extensions, geographic expansion, and new channel development. Furthermore, they have increased margins at acquired companies through operational improvements and leveraging revenue growth. For instance, The North Face, Vans, and Timberland all had operating margins below 10% at the time of acquisition versus in the mid-teens today.

While they have had some home run acquisitions over the years, they are also not afraid to divest and spin off low-growth brands. They divested the Vanity Fair Intimates business (for which VF Corp. is named) in 2007, the Contemporary Brands businesses in 2016, the Licensed Sports Group business in 2017, and Nautica in 2018. Then, most recently, they spun off the Jeans business in 2019 (~18% of revenue).

The chart below highlights some of the major acquisitions over the years:

Source: Company Presentation

Remaining VF Corp.

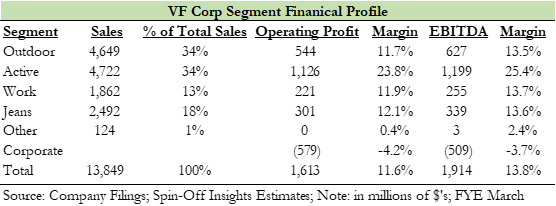

As discussed, VF Corp. has been very successful in actively managing the portfolio to grow the business over time. After the Jeans spin-off, named Kontoor Brands (KTB), VF Corp.'s four main brands are The North Face, Timberland, Vans, and Dickies. The North Face and Timberland are included in the Outdoor segment, Vans is part of the Active segment, and Dickies makes up a large part of the Work segment.

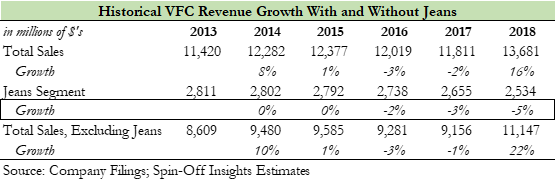

VF Corp.'s historical revenue growth is a little difficult to evaluate because of all the acquisitions and divestitures over the years. However, as you can see in the table below, the Jeans business has been shrinking which has lowered VF Corp.'s consolidated growth rate.

Going forward, VF Corp. is a more focused, faster-growing, and higher margin business where management can spend more time looking for growth opportunities rather than managing the Jeans segment turnaround (exposure to the struggling wholesale channel has hurt).