Summary

- Bank of America’s 2018 CCAR (Comprehensive Capital Analysis and Review) was a disappointment, in our view.

- For the 2019 DFAST (Dodd-Frank Act Stress Tests), we expect Bank of America's hypothetical stressed CET1 minimum ratio to be slightly below the 2018 DFAST level.

- Still, it will be a good DFAST outcome, in our view, which will allow the bank to raise dividends.

- We expect a 30% DPS hike from Bank of America.

- Looking for more? I update all of my investing ideas and strategies to members of Banking On Financials. Start your free trial today »

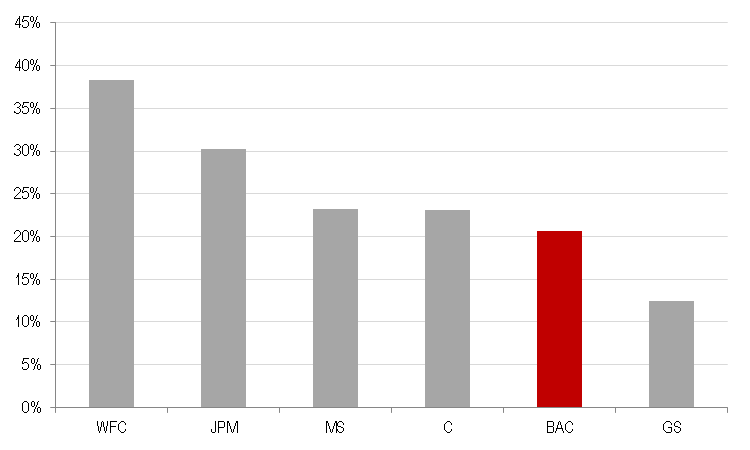

Bank of America (BAC) disappointed investors with its 2018 CCAR release, in our view. Despite the strong 2018 DFAST results, which were one of the best among large-cap U.S. banks, a well-capitalized balance sheet, and a strong rise in earnings, Bank of America increased its dividend only by 25%, from a quarterly DPS of $0.12 to $0.15. We had expected a higher increase, especially given BAC’s low dividend payout ratio. Notably, even after this 25% hike, BAC has the second-lowest payout ratio among the big-6 US banks, and the lowest one if we exclude investment banks. It’s also worth noting that the Fed gave a conditional non-objection to Goldman Sachs (GS) and Morgan Stanley (MS), and, as a result, they had to limit their capital distributions. By contrast, BAC received clear approval from the Fed.

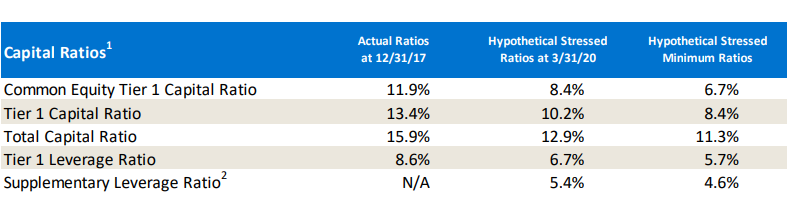

Bank of America: 2018 DFAST results

Source: Company data

Big-6 US banks: Dividend payout ratio

Source: Companies data, Bloomberg

BAC and the 2019 DFAST assumptions

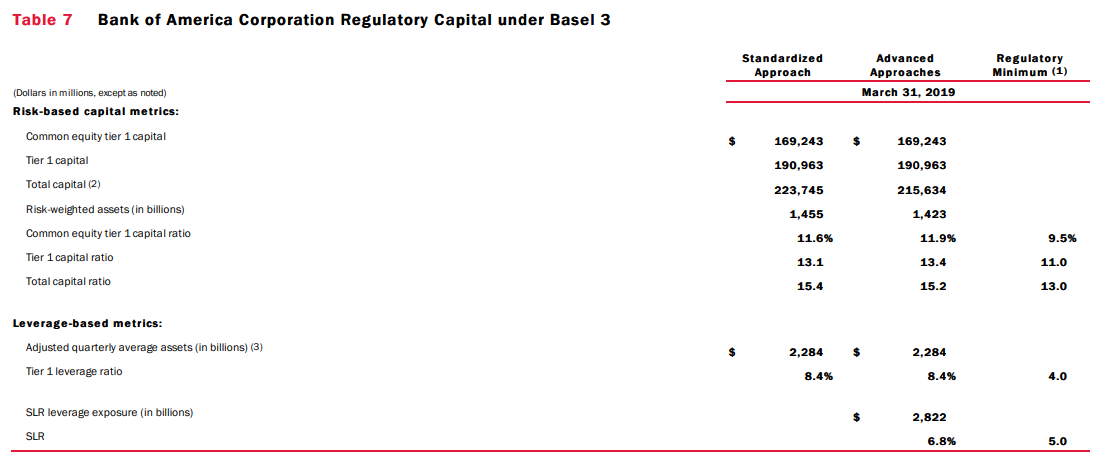

As shown below, BAC’s minimum CET1 requirement is 9.5%. That includes a basic minimum of 4.5%, the 2.5% capital conservation buffer and the 2.5% G-SIB surcharge. As of March 2019, its CET1 was 11.6% and 11.9% under the standardized approach and advanced approaches respectively. The SLR (supplementary leverage ratio) was 6.8%.

Source: Company data

The 2019 DFAST severely adverse scenario features a lower decline in asset prices (equity, home, and commercial real estate prices). That should be a positive not only for investment banks but also for BAC’s trading division and asset quality of its mortgage/commercial real estate portfolios. This lower decline is attributed to quite a significant drop in UST yields. To recap, the 2018 DFAST featured stable UST yields and a steeper yield curve. As a result, the 2019 DFAST will have a more negative impact on BAC’s net interest margin. Another difference between the 2019 and the 2018 DFAST, which is important for BAC and other banks with exposure to consumer loans, is that the 2019 DFAST severely adverse scenario features a higher increase in the US unemployment rate and a sharper decline in the country's GDP compared to the 2018 assumptions.